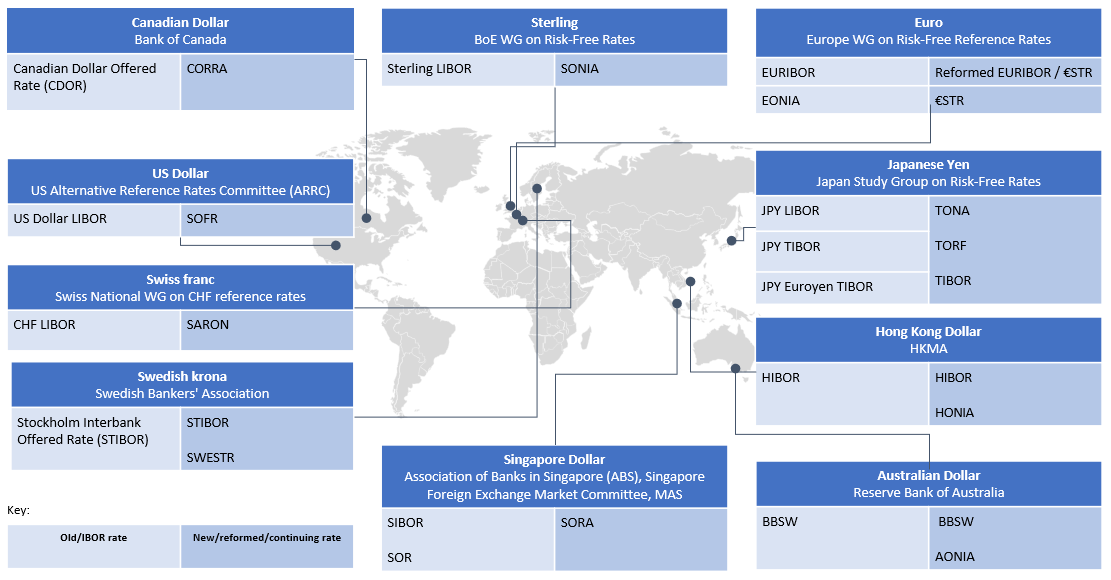

LIBOR cessation

All settings (including synthetic settings) of LIBOR have now ceased. For more information see the joint statement (October 2024) on the end of LIBOR from the Bank of England, FCA and Working Group on Sterling Risk-Free Reference Rates.

For other (non-LIBOR) rates, see the relevant sections below.

EURIBOR

EURIBOR is not scheduled to be discontinued. The working group on euro risk-free rates has made recommendations on fallback rates - see the EURIBOR and EONIA transition section below for more information.

Term SOFR

While Term SOFR is available for use, it requires entry into a license for certain cases and is subject to limited scope of use recommendations.

Contracts which continue to reference LIBOR

English law legislative solution for Tough Legacy Contracts

The Critical Benchmarks Act (see our briefings Synthetic LIBOR and contractual continuity and 10 things you need to know about synthetic LIBOR and the Critical Benchmarks Act) essentially provides that references to LIBOR in English law contracts will be read as references to LIBOR as it continued to be published under the changed methodology (synthetic LIBOR). This legislation is now of limited use since all LIBOR settings have ceased.

Parties to contracts which continue to reference LIBOR should take actions necessary to determine the applicable fallback rates and a replacement of USD LIBOR since all LIBOR settings have now ceased.

US law legislative solution for Tough Legacy Contracts and use of synthetic USD LIBOR

Effective 3 July 2023, the US Adjustable Interest Rate (LIBOR) Act as implemented by Regulation ZZ supplies a replacement benchmark for USD LIBOR by operation of law in contracts governed by US law (includes the laws of each US state, such as New York law) if the contract lacks adequate fallback provisions or a person authorized to select a replacement benchmark failed to do so. For most business contracts (that are not derivatives) the replacement provided pursuant to the LIBOR Act is the equivalent tenor of Term SOFR plus the applicable tenor spread adjustment.

Legacy contracts and financial instruments that refer to USD LIBOR but are outside the scope of the US LIBOR Act (for example, because a contract contains a fallback to a workable benchmark rate in the event of a market disruption event) and that do not include a fallback transition trigger related to the representativeness of USD LIBOR may refer to synthetic USD LIBOR rates (this requires case-by-case review of the relevant contractual definition of USD LIBOR). Parties to these contracts or financial instruments should consider taking actions necessary to determine a replacement for USD LIBOR by 30 September 2024, which is when publication of synthetic USD LIBOR settings is expected to cease.

For USD LIBOR swap rates, see LIBOR transition: US Dollar below.

Product areas

Recommended replacement rates vary by jurisdiction and calculation methodologies continue to develop and vary by product. Trade and other associations have worked and continue to work with the relevant jurisdiction and currency specific working groups on transition issues pertinent to their specific products, to ensure appropriate consistency for linked products and, where necessary, to update their documentation to accommodate alternative benchmark rates - see trade and industry bodies below.